Pros And Cons of Affirm: What You Need to Know Before Using It

Buying what you want and need has changed a lot in recent years. Many shoppers now use buy now, pay later services when shopping online or even in stores. One of the most popular services is Affirm. If you are thinking about using Affirm, you probably want to know if it is a good choice. This article will help you understand the pros and cons of Affirm in simple language, with real examples, so you can decide if it fits your needs.

Affirm lets you split your purchases into smaller payments over time, instead of paying everything at once. It is available at many online stores and some physical shops. While it can make shopping easier, there are important things to consider before you use it.

We will look at how Affirm works, its main advantages, and the possible downsides. You will also learn about common mistakes, who benefits most, and what to watch out for to avoid trouble.

How Affirm Works

Affirm is a buy now, pay later (BNPL) platform. It lets you buy items and pay for them in installments, often with no hidden fees. You will see the payment schedule and total amount upfront before you agree. Many people like Affirm because it is easy to use and helps them manage their cash flow.

Here is how a typical Affirm transaction works:

- You shop at a store that offers Affirm as a payment option.

- At checkout, you select Affirm and fill out a quick application.

- Affirm checks some information about you, often including a soft credit check.

- If approved, you choose a payment plan (sometimes 3, 6, or 12 months).

- You make payments to Affirm, not the store.

Affirm may charge interest on longer payment plans, but some merchants offer zero-interest deals. There are no late fees, but missing payments can still hurt your finances.

Pros Of Affirm

Affirm offers several benefits for shoppers. Let’s explore the main advantages and some details that are often missed.

1. Simple And Transparent Payment Plans

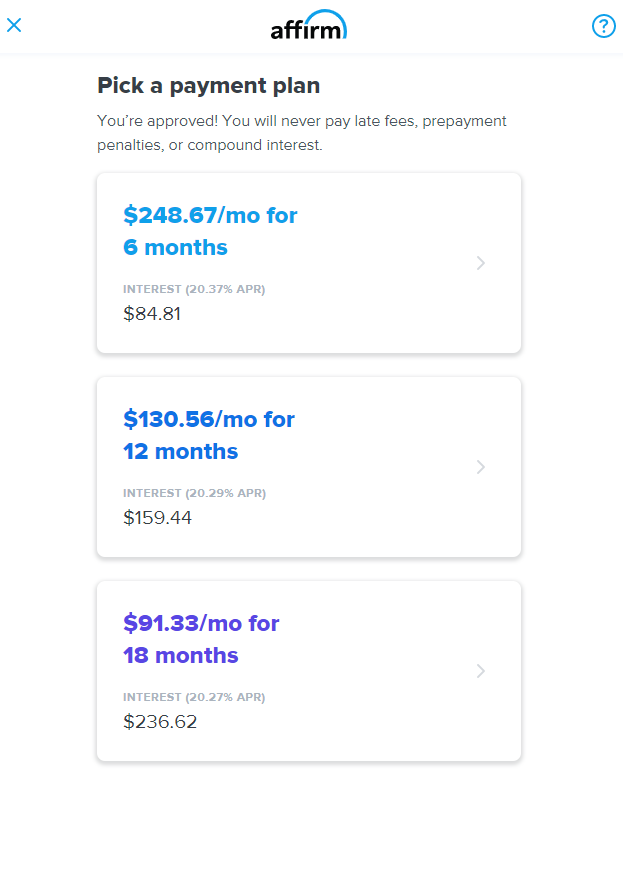

One of the biggest advantages of Affirm is transparency. When you use Affirm, you see the full payment schedule and total amount before you agree. This is different from credit cards, where interest can be confusing and costs can rise quickly if you do not pay in full. Affirm does not have hidden fees, and you always know exactly how much you will pay.

For example, if you buy a laptop for $600 and choose a 6-month plan with no interest, you pay $100 every month. If there is interest, Affirm shows you the total cost upfront. This makes it easier to plan your budget and avoid surprises.

2. No Hidden Fees Or Late Fees

Affirm does not charge late fees or prepayment penalties. If you miss a payment, you will not be charged extra. This is different from many other BNPL services and credit cards, which often have high late fees. While this does not mean you should miss payments, it does provide some peace of mind if you forget or have a problem one month.

3. Quick Approval Process

The application process for Affirm is fast and simple. You do not need a long application form or lots of documents. Most people get an answer in seconds. Affirm uses a soft credit check that does not affect your credit score. This makes it easy to see if you qualify without worrying about hurting your credit.

4. Flexible Payment Terms

Affirm offers several repayment options. You can often choose between different plans, such as paying in 3, 6, or 12 months. Some stores offer even longer terms. This flexibility helps you pick a plan that matches your budget.

Here is a simple comparison of sample Affirm plans:

| Purchase Amount | 3-Month Plan | 6-Month Plan | 12-Month Plan |

|---|---|---|---|

| $300 | $100/month | $50/month | $25/month |

| $600 | $200/month | $100/month | $50/month |

If you want to pay off your loan early, you can do so without any penalty.

5. No Minimum Credit Score Required

Many BNPL services have strict rules about credit. Affirm is more flexible. You do not need a high credit score to be approved. Some people with no credit history or a low score can still use Affirm. However, approval is not guaranteed, and terms may be less favorable for those with bad credit.

6. Works With Many Merchants

Affirm partners with thousands of retailers. You can use it to buy electronics, clothing, travel, furniture, and more. This wide acceptance makes it convenient for different types of purchases.

For example, you can use Affirm at brands like Peloton, Adidas, Target, and Expedia, among many others.

7. Helps With Budgeting

Since you know your exact payments and when they are due, Affirm can help you manage your money. It is easier to avoid overspending because you see the total cost upfront. This is useful if you have a fixed income or want to avoid debt surprises.

8. No Compound Interest

Affirm charges simple interest on loans (when interest applies), not compound interest. This means you only pay interest on the original loan amount, not on top of interest already owed. With credit cards, interest compounds and can grow quickly if you do not pay in full.

For example, if you borrow $1,000 at 10% simple interest for one year, you pay $100 in interest. With compound interest, the cost could be higher.

9. Easy To Track Payments

Affirm’s app and website make it easy to track your payments. You get reminders, can view your schedule, and see your balance at any time. This helps you stay organized and avoid missed payments.

10. May Improve Your Credit Mix

Using Affirm can add to your credit mix if Affirm reports your loan to credit bureaus. Having different types of credit (loans, credit cards, etc.) can be positive for your credit profile. However, not all loans are reported, and this is not a guarantee.

11. Safe And Secure

Affirm uses encryption and other safety measures to protect your data. Your personal and payment information is kept secure, and you do not need to share your credit card details with merchants.

12. Can Help Build Credit (in Some Cases)

If Affirm reports your payments to credit bureaus, making on-time payments can help build your credit history. This is especially helpful if you are new to credit or rebuilding your score. However, this benefit is only for loans that Affirm chooses to report.

13. No Revolving Debt Trap

Affirm’s loans are installment loans with a set payoff date. This is safer than a credit card, where you can carry a balance for years and pay high interest. With Affirm, your debt will end when you finish your last payment.

14. Suitable For Large And Small Purchases

You can use Affirm for both small items (like shoes) and big-ticket items (like a mattress or bike). This makes it flexible for many situations.

15. Real-time Approval Decision

You do not have to wait days for approval. Affirm gives you a decision almost instantly, which is convenient when shopping online or in a store.

Credit: www.creditcards.com

Cons Of Affirm

While Affirm has many strengths, there are also important downsides and risks to consider. Some of these may not be obvious at first.

1. Interest Charges Can Be High

Affirm does not always offer zero-interest plans. If you do not qualify for a 0% deal, the interest rates can be much higher than you might expect. Rates can reach up to 30% APR or more, depending on your credit and the merchant.

Here is a comparison of a zero-interest plan and a plan with interest:

| Loan Amount | 0% Interest | 15% Interest |

|---|---|---|

| $500 (6 months) | $83.33/month | $89.92/month |

| Total Paid | $500 | $539.52 |

This means you could pay much more than the original price, especially for longer plans.

2. Temptation To Overspend

Because Affirm makes it easy to pay in small pieces, it can be tempting to buy more than you can afford. People sometimes choose bigger or extra items because the monthly payment seems small. This can lead to debt problems if not managed carefully.

3. Missed Payments Hurt Credit

While Affirm does not charge late fees, missed payments can still have serious consequences. If Affirm reports your loan to a credit bureau, late or missed payments can damage your credit score. Even if there are no fees, the impact can last for years.

4. Not All Purchases Qualify

Some items or stores do not allow Affirm payments. There are also minimum and maximum loan amounts. For example, you might not be able to use Affirm for a $15 item or a $10,000 purchase. It depends on the merchant and Affirm’s decision.

5. No Rewards Or Cash Back

Unlike many credit cards, Affirm does not offer rewards points, cash back, or travel perks. You only get the ability to pay over time. If you use a rewards credit card and pay in full, you might actually save or earn more than with Affirm.

6. Limited Credit Building

While Affirm loans can help your credit, this is not always the case. Affirm does not report all loans to credit bureaus. Short-term, zero-interest loans may not appear on your credit report. This means you could be making payments, but your credit score does not benefit.

7. Refunds Can Be Complicated

If you return an item bought with Affirm, the refund process can take time. You may have to keep making payments until the store confirms the return and Affirm cancels the loan. This can be confusing and frustrating for some shoppers.

8. Not Always Cheaper Than Credit Cards

If you have a credit card with a low or zero interest rate, Affirm may cost more. Some cards offer 0% interest for new purchases for a set time. Affirm’s interest charges can be higher unless you get a special deal.

9. Approval Is Not Guaranteed

Not everyone is approved for Affirm. If you have bad credit or not enough income, Affirm may decline your application. This can be disappointing if you were counting on using it.

10. Payment Dates Are Fixed

Affirm’s payment schedule is set when you agree to the loan. If your income or situation changes, it is hard to change your due date. Some users find this less flexible than a credit card, where you can pay a minimum amount if needed.

11. Potential For Multiple Loans

Since Affirm is easy to use, some shoppers end up with several loans at once. This can make it hard to keep track of payments and increase the risk of missing one.

12. Does Not Build Long-term Credit History

Short-term Affirm loans, especially those not reported to credit bureaus, do not help you build a long credit history. A long credit history is important for better credit scores in the future.

13. May Not Cover All Locations

Affirm is widely available online, but not every physical store accepts it. If you shop in person often, you might not be able to use Affirm everywhere.

14. Some Services And Products Excluded

Affirm does not allow purchases of certain goods or services. For example, you cannot use Affirm for gambling, illegal items, or some types of gift cards. The list can change, so it is important to check before shopping.

15. No Option To Skip Payments

If you have a tough month, Affirm does not allow payment holidays or skipping a payment without consequences. You must pay on time, or your credit could suffer.

Real-world Examples

To better understand the pros and cons, let’s look at some real situations:

- Maria bought a $1,200 exercise bike with Affirm. She chose a 12-month plan at 0% interest, paying $100 each month. She found it easy to budget and paid off her loan with no extra cost.

- David used Affirm for a $500 TV but did not realize his plan had a 20% interest rate. Over 12 months, he paid $550 in total—$50 more than the sticker price. He later discovered he could have used his 0% credit card instead.

- Sophie bought several items using Affirm. She liked the small payments but lost track of how many loans she had. When her income dropped, she missed a few payments, and her credit score dropped.

These examples show that Affirm can be helpful, but only if you use it wisely and read the terms carefully.

Credit: www.businessinsider.com

Who Should Use Affirm?

Affirm is best for certain types of shoppers:

- People who need to spread out payments for a big purchase and want to avoid credit card debt.

- Those who want simple, fixed payments with no hidden fees.

- Shoppers who do not have access to low-interest credit cards.

- People who need to buy something important and cannot pay all at once, but can afford the monthly payments.

Affirm is not a good fit for:

- People who are likely to overspend or have trouble managing debt.

- Those who already have low-interest credit cards and pay their balance in full.

- Shoppers looking for rewards, cash back, or travel points.

- Anyone who cannot commit to regular, on-time payments.

Common Mistakes To Avoid

Many new users make mistakes with Affirm. Here are important tips:

- Ignoring the interest rate: Always check if your plan is 0% or has interest. Even small interest adds up.

- Forgetting about multiple loans: If you use Affirm often, keep a list of all your loans and payment dates.

- Missing payments: Even without late fees, missed payments can hurt your credit.

- Not reading the terms: Each loan can have different rules. Always read before you agree.

- Using Affirm for wants, not needs: Affirm can make shopping easier, but do not use it to buy things you do not really need.

Comparing Affirm With Other Payment Methods

Let’s see how Affirm compares to credit cards and other BNPL services:

| Feature | Affirm | Credit Cards | Other BNPL |

|---|---|---|---|

| Interest Charges | Simple, upfront | Compound, can be high | Varies, sometimes hidden |

| Late Fees | No | Yes | Often Yes |

| Rewards/Cash Back | No | Yes | Rarely |

| Credit Impact | Possible | Yes | Varies |

| Approval Speed | Instant | Usually instant | Instant |

| Reporting To Credit Bureaus | Sometimes | Yes | Rarely |

Non-obvious Insights

Here are two key insights many beginners miss:

- Interest is not always zero: Many people assume all Affirm plans are zero-interest. In reality, only some offers have 0%. Always check your offer carefully.

- Soft credit checks can still affect future credit: While Affirm’s soft checks do not lower your score, having many BNPL accounts can affect your ability to get other loans if lenders see you have lots of short-term debt.

How To Use Affirm Wisely

If you decide to use Affirm, here are some smart strategies:

- Only use Affirm for important purchases you cannot pay for in full.

- Choose the shortest repayment plan you can afford to reduce interest.

- Track all your Affirm loans in a notebook or app.

- Set reminders for payment dates to avoid missing them.

- Compare Affirm’s costs with credit cards or other payment options.

- Read all terms and details before you click "agree."

Is Affirm Safe?

Affirm uses strong encryption and privacy practices to keep your information safe. It is a large, well-known company. However, you should always protect your login and personal data. If you have a problem, Affirm’s customer service can help, but resolving some issues (like refunds) may take time.

For more information about BNPL safety, you can visit the Consumer Financial Protection Bureau.

Credit: www.skylineschool.net

Frequently Asked Questions

What Credit Score Do I Need To Use Affirm?

There is no set minimum credit score for Affirm. Many people with fair or average credit are approved. Approval depends on your income, payment history, and the amount you want to borrow. Sometimes, even people with no credit can qualify.

Does Affirm Report To Credit Bureaus?

Affirm sometimes reports loans to credit bureaus, but not always. Long-term loans and loans with interest are more likely to be reported. Short-term, zero-interest loans usually are not. Check the details of your loan if this is important for your credit.

What Happens If I Miss A Payment With Affirm?

If you miss a payment, Affirm does not charge a late fee. However, missed payments may hurt your credit if your loan is reported to a bureau. Affirm may also block you from using its service again until you pay what you owe.

Can I Pay Off My Affirm Loan Early?

Yes, you can pay off your loan early without any penalty. Doing so can save you money on interest if your plan has interest charges. You can make extra payments anytime through the Affirm app or website.

Is Affirm Better Than A Credit Card?

Whether Affirm is better than a credit card depends on your needs. Affirm is good for fixed payments and transparency, especially if you get a zero-interest plan. Credit cards offer rewards and more flexibility, but can be more expensive if you do not pay in full. Compare both options before you decide.

---

Affirm can be a helpful tool for spreading out payments and managing your budget. It offers clear terms, no hidden fees, and a simple process. However, it is not risk-free. High interest, the temptation to overspend, and possible credit impacts are important to consider. If you use Affirm, do so wisely and always read the details. By understanding the pros and cons of Affirm, you can make better choices and avoid common mistakes.

{kind=link}